Hate to break this news to you younger folks, but things get more difficult once you’re a senior citizen like me. I know, you’re familiar with stories of hearing difficulties, driving at night. opening jars with twist tops, and remembering where you put your damn reading glasses.

There’s lesser known troubles, though. Here’s one that I encountered today.

Two facts collided. One was that I turned 77 last month. The other was that I needed to renew my subscription to New Scientist magazine, a weekly published in Great Britain that I like a lot.

Usually I renew for another year. This time I paid more attention to a bold-faced message in the Renew Now letter I got: Your subscription is due to expire on 20 December 2025. Secure a 1 year renewal for $299.00 — a 26% saving — or unlock a free year with our 3-year offer.

The 3-year offer had a price tag of $598. Even without a calculator I could figure out that two times $299 is $598. So if I took New Scientist up on the 3-year offer, I would indeed get a free additional year for the price of two years.

A really good return on my $598 investment, 50% I believe. Way better than I’d get from a money market fund, or even the stock market. But then I thought…

Am I going to live another three years? What if I don’t? At my age, maybe I should limit myself to one-year subscription renewals, especially since my wife isn’t as enamored with New Scientist as I am, and probably would prefer to be reading articles about how to live life to the fullest after your husband dies.

Initially uncertain about what to do, it didn’t take long for my desire to save money outweighing my fear of not outliving a 3-year New Scientist subscription. I logged into my online account and sent off $598 via PayPal.

Belatedly, I realized that a more pleasingly scientific approach would have been to consult a life expectancy calculator and see whether I had considerable leeway in living at least as long as three additional years.

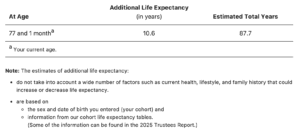

I’d used the Social Security calculator before, which only asks when you were born. I was encouraged when the result was 10.6 years of additional life expectancy.

Reading the fine print, though, made me realize that lifestyle does indeed play a significant role in how long people live. So I fired up a John Hancock life expectancy calculator for a more refined estimate of my death date.

It wanted to know my height and weight (5’10, 167), how often I exercised (every day), how often I drink alcohol (never, or very rarely), how many driving violations I had in the past year (zero), how my blood pressure and cholesterol level are (both normal), whether I smoke (no, tobacco at least), and my sex (male). The result:

Wow. Even if I don’t finish reading all of the New Scientist issues within three years. if I live to 102 I’ll have plenty of time to do that. Well, assuming I don’t suffer from blindness or dementia.

Actually, the prospect of living to 102 doesn’t fill me with joyful anticipation — even though it’s good news from the standpoint of buying 3-year magazine subscriptions. Eighty-seven seemed closer to ideal, though 90 has a nice round number feel to it: really old, but not totally decrepit old.

Anyway, now I know that statistically speaking, I’m OK with renewing subscriptions for ten years. Heck, 25 years if John Hancock is correct. Now I can relax when renewal notices arrive. After all, stress isn’t conducive to living a long life.

Discover more from Hinessight

Subscribe to get the latest posts sent to your email.